State of the Circle - March 2026 EPR Readiness Circle

CIRCLE BY OPLN

EPR Readiness Circle | State of the Circle

March 2026 Session Synthesis — Executive Briefing

On March 17, 2026, Circle by OPLN convened a cross-industry cohort of obligated producers, trade associations, consultancies, and producer responsibility organizations for its inaugural EPR Readiness Circle. Through anonymous pre-session polling and a structured ninety-minute discussion, the session surfaced a clear picture: the industry is engaged, increasingly informed, and potentially under-equipped to accurately forecast the impact of at-risk formats under SB54.

1. Flexible Packaging Is the Industry’s Central Vulnerability

Sixty-two percent of respondents identified flexible formats—snack wrappers, pouches, sachets, and frozen food bags—as their highest exposure category under SB 54. Fiber portfolios followed at 23%, with compostable plastics at 15%. The factors driving this exposure are systemic: fee uncertainty and redesign timeline constraints (both 55%), supplier limitations (45%), and a cluster of infrastructure gaps—limited curbside acceptance, contamination during sorting, MRF screening loss, and weak end markets—each cited by 45% of participants.

2. Financial Modeling Confidence Remains Low

Zero percent of respondents reported high confidence in modeling eco-modulated fee exposure. The majority—54%—operate on rough assumptions only, while 15% have no ability to model at all. Discussion participants reinforced this: fee schedules exist only for Colorado and Oregon, leaving California’s eco-modulation framework largely theoretical. The gap between regulatory timeline and organizational readiness to quantify financial impact is significant and widening.

3. Supplier Engagement Has Only Just Begun

Thirty-eight percent of respondents are still assessing portfolio impact internally; another 38% have initiated preliminary supplier conversations. Twenty-three percent have begun updating internal specifications. No respondents have communicated updated requirements to suppliers or transitioned formats. With packaging redesign timelines measured in years—participants noted some fresh-cut produce formats are estimated at fifteen years from viable alternatives—the disconnect between compliance deadlines and material reality is a structural tension the industry has not yet resolved.

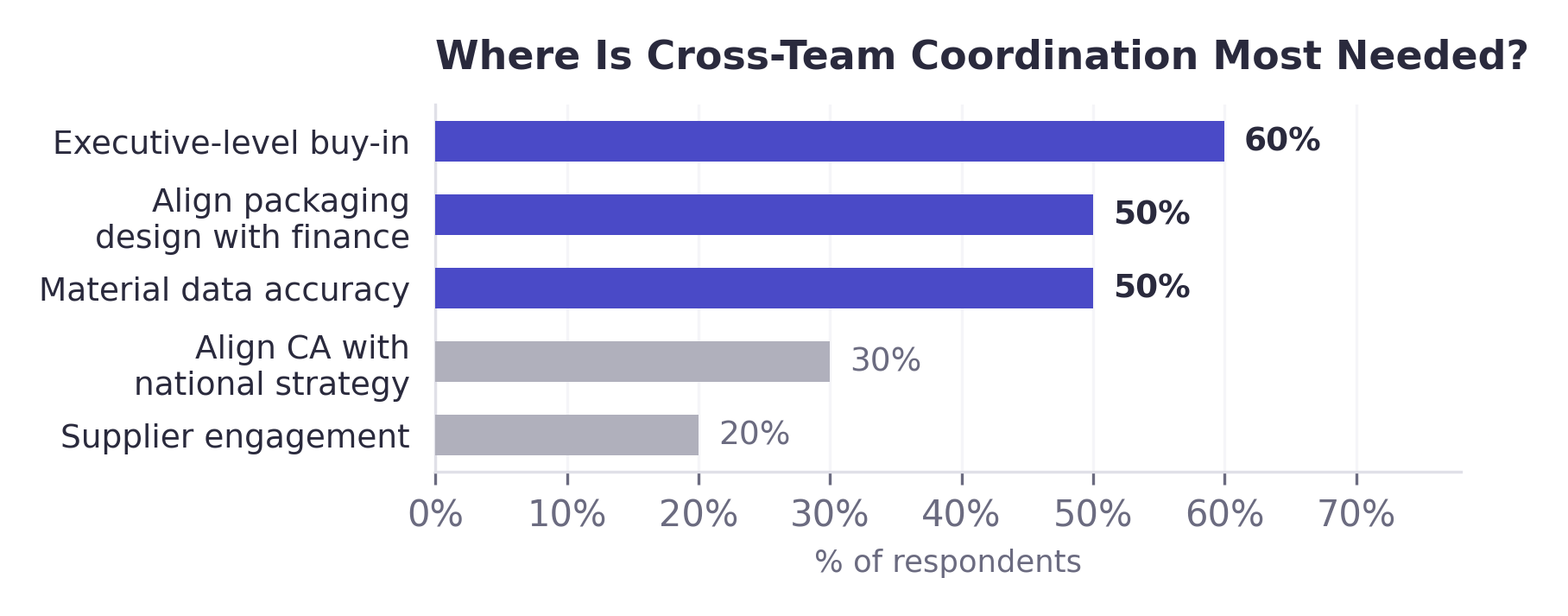

4. The Biggest Internal Challenge Is Getting Leadership to the Table

Sixty percent of respondents identified building executive-level buy-in as their top cross-team coordination priority—surpassing even aligning packaging design with financial modeling (50%) and improving material data accuracy (50%). The practitioners closest to the work are signaling that the constraint is not knowledge or intent, but organizational prioritization.

Implications for Leadership

First, the financial exposure from packaging EPR is real, imminent, and poorly quantified across the industry. Second, flexible packaging represents a systemic risk that cuts across material science, infrastructure, and regulatory design. Third, the supplier engagement pipeline is almost entirely unfilled. Fourth, the practitioners leading EPR readiness are asking for what only senior leadership can provide: organizational priority, cross-functional authority, and investment in early-action piloting.

Anonymized, aggregate findings from the March 2026 EPR Readiness Circle convened by Circle by OPLN. Please note the results shown reflect the experience of attendees but are not generalizable.

Subscribe to Circle Newsletter

Join thousands of leaders shaping circular policy. Get insights delivered.